Retail Banking – Greater customer proximity for sales, marketing and service

In times of increasingly dynamic markets and heterogeneous target groups, customer experience has become a strategic challenge for institutions. Building and maintaining lasting, efficient customer relationships through positive customer experiences is of central importance.

At msg for banking, we focus on innovative customer-oriented solutions, user-centred design, lean product development and new technologies for financial service providers.

Make an appointment for advice

Let our CX experts show you how your company can build customer relationships efficiently and sustainably. Seize the opportunity and arrange your 30-minute consultation now – free of charge and with no obligation, of course!

Our Vision

By taking a close look at your ecosystem and using our creativity to design practical solutions for your customers and consultants throughout the entire customer journey, we help you shape your business future in innovative ways.

Insurance pilot for banks

The future of insurance sales in financial institutions

Identify customer needs and offer tailor-made solutions with the insurance pilot for banks.

Whitepaper: Bancassurance

What makes bancassurance successful?

Solutions and insights from real-world experience. Download the white paper for free!

Study: Customer Touchpoints

Customer touchpoints in banking

Recommendations for an optimal customer experience. Download the study for free!

Our service portfolio for customer-oriented banking with added value

Development of sales- and market-oriented growth and transformation strategies and solutions

The new, digitally driven market for financial products presents many challenges and opportunities. We help you identify these and continue to offer your customers the service they expect in the future.

Specific services:

- Analysis and evaluation of current sales processes/channels and market and marketing factors

- Design of digital sales, products and services

- Development and evaluation of implementation scenarios

- Implementation, support and introduction

Your added value:

- Change/adaptation of the organisation to new market requirements

- Omnichannel sales orientation

- Optimal alignment of products to the market

- Increased customer loyalty (NPS improvement)

- Fast market effectiveness (time-to-market)

- Innovation leadership

Digitalisation of the customer journey (customer interfaces and corresponding applications from a user and benefit perspective)

Customer focus is a key competitive factor. We examine and benchmark your applications and work with you to develop solutions for an even more customer-friendly future.

Specific services:

- Analysis and evaluation of customer processes from the user's perspective and business value of the company

- CX design/co-creation of a user-oriented ideal process

- Development of a technical solution and system selection

- Implementation and testing

- Conversion optimisation

Specific topics:

- Application process for credit/mortgage financing

- Bancassurance

Your added value:

- More efficient processes – Lower internal IT resource utilisation

- High performance/availability of systems

- Higher conversion rates

- High flexibility/A/B testing mindset

Optimising customer advice using digital solutions

Personal advice remains a fundamental component. Digital systems help to optimise this contact for both customers and advisors. We support you in identifying value-adding processes and finding the right tools.

Specific services:

- Analysis and evaluation of the current advisory process from the customer's perspective (accessibility, understanding, transparency of offers, processes (signature), follow-up, conversion

- Design of solutions + tools for simplification + optimisation

- Implementation of KPI systems for measuring success

Your added value:

- Shorter onboarding times for new employees

- Increased customer satisfaction for sustainable consulting

- Increased conversion rate in the sales process

Data-driven optimisation of lead management, lead conversion and customer loyalty programmes

Leads and opportunities represent potential for additional/follow-up business. We identify potential in your business model and develop ideas and concrete solutions for greater value creation.

Specific services:

- Analysis of existing lead flows and lead management

- Development of measures for targeted lead acquisition and increased value creation

- Tech advice: Creation of solution concepts for software and architecture

- Implementation of lead/CRM software and connection to existing systems/data

- Education, training and change management

- Content and UX development of CRM assets

- KPI set definition

Your added value:

- Increased interaction between customers and the company

- Reduction in cancellations/cancellation rates

- Increased brand loyalty

- Increased cross-selling/up-selling rates

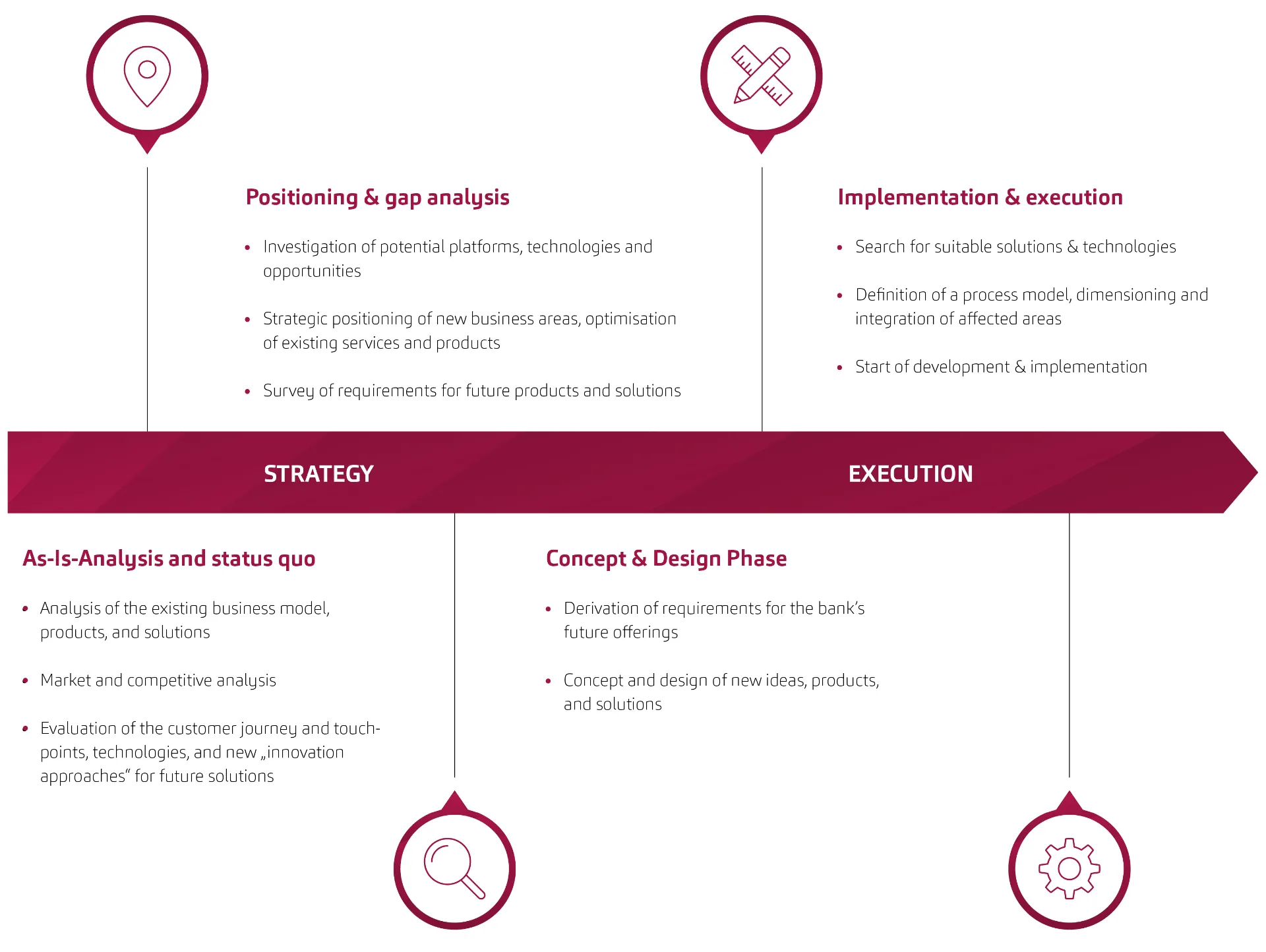

Our process model

Our service portfolio for your bancassurance sales

With our expertise in both banking and insurance, we offer you solutions for a successful bancassurance business – from identifying suitable cooperation partners to sales implementation on the banking platform.

Bancassurance status analysis and identification of business opportunities

Outcome:

- Overview of current status (products, sales, technology)

- Potential

- Measures

Inventory activation

Value for the customer:

- Increase in sales/conversion rates with insurance products

Implementation:

- Holistic conception and design of customer communications across all relevant touchpoints and banking channels

Market demand + insights:

➔ Many partnerships have been established, but the desired sales effect is lacking

Discover our Insurance Pilot – the modular solution and smart extension for your financial institution that allows you to integrate tailor-made

insurance solutions directly into your banking platform and strengthen your customer relationships in the long term.

Product portfolio + product strategy

Value for the customer:

- Increase in product fit / development of financial innovations

Implementation:

- Development of a sales channel and target group-specific product portfolio that can be optimally integrated into the existing customer and sales structure

Market demand + insights:

➔ Currently, almost exclusively standard products from insurers are being used. There is a lack of tailored solutions.

Technical connection/integration

Value for the customer:

- Expansion of the company's own product portfolio to include insurance

Implementation:

- Seamless integration of both process worlds for customers and sales

Market demand + insights:

➔ Connecting banking and insurance systems is a very complex task. Fast and flexible solutions are sought.

msg for banking is your reliable partner with all the relevant skills for the banking of the future.

Industry expertise

Decades of experience in consulting and implementing complex projects and processes in the banking landscape of the DACH region

Best advice

Partnerships and implementation expertise with relevant providers for data and process management

UX/UI

Award-winning research and UX unit with a focus on financial services

Cloud strategy

Active partnerships with all major hyperscalers and consulting in the regulatory environment.

Artificial intelligence

AI competence team and cooperation with relevant AI manufacturers.

Your contact persons

heads up the Financial Services division at msg for banking, which focuses on digital, customer-centric solutions for the financial industry.

is a CX expert specializing in customer-oriented sales processes and CRM strategies. At msg for banking, he advises customers on all stages of the digital sales funnel and digitally supported consulting.