Successfully managing capital as a key success factor for banks!

ICAAP, ILAAP, IRRBB, CRR III......

For several years now, regulation in capital and financial management has focused on ensuring the resilience of banks in the national and international environment.

It has become clear that, when it comes to management, leveraging the implementation synergies of individual topics is particularly crucial for banks to make economic use of regulatory requirements. In doing so, the connection between planning, risk management, and reporting must be pursued as a holistic approach in terms of expertise, technology, and processes.

Let's leverage this potential together with our partnership-based approach!

CRR III – the new KSA

The new CRR regulations increase capital requirements for KSA institutions. What aspects are changing and what does this mean in concrete terms for the banks and savings banks affected?

Service offering

ICAAP ensures economic risk-bearing capacity (Pillar II) and requires strategic management of capital reserves in line with objectives and market conditions—we support you with tools and advice.

The normative perspective of ICAAP focuses on compliance with regulatory requirements (Pillar I) through sound capital planning. Institutions must proactively plan their future earnings forecasts and capital adequacy in order to meet all regulatory requirements at all times.

This requires regular review and adjustment of the assumptions and parameters used. With our integrated solutions, we support you in efficiently implementing all relevant requirements.

The ILAAP ensures that institutions can effectively manage their liquidity risks and maintain their solvency even under stress conditions. Scenario analyses and robust planning processes ensure long-term resilience to liquidity shocks. We offer customized approaches to help you optimize your liquidity management.

The new requirements for IRRBB scenarios focus on more precise calibration of interest rate shocks for all relevant currencies. Advanced scenario analyses enable institutions to forecast the effects of interest rate changes more accurately and optimize their management tools. With our holistic approach, we support you in designing your interest rate shock scenarios with precision.

Regulatory requirements such as IDW RS BFA 3 are increasingly influencing accounting valuations. Interest rate reversals, hidden reserves, and refinancing costs require flexible valuation curves—our experts provide you with strategic and future-proof support.

A key challenge in breaking down net interest income into its individual components, such as margin contribution, maturity transformation result, and refinancing costs, is to use adequate market values and yield curves for the valuation, as different assumptions can lead to distortions. Implementation requires robust systems, clear internal guidelines, and transparency in order to correctly reflect the split from both an accounting and risk management perspective. We support you in this with customized approaches to implement the split of results and your strategic goals.

Asset-backed securities offer financial institutions an efficient way to optimize capital and meet regulatory requirements. By transferring high-risk portfolio components to investors, institutions can reduce their risk-weighted assets and thus free up capital. With our expertise, we provide you with comprehensive support—from transaction structuring to automated reporting.

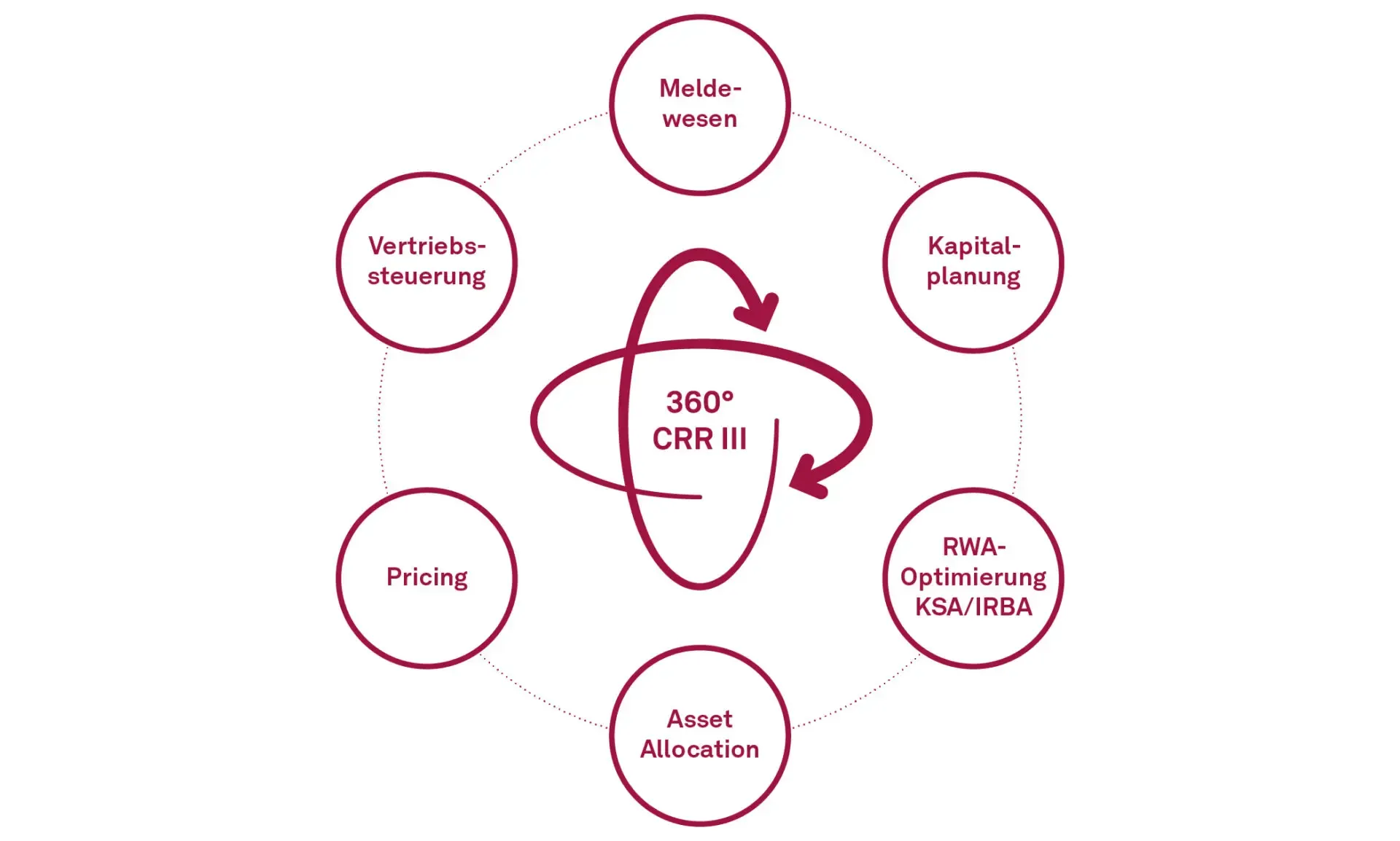

The introduction of CRR III brings comprehensive changes, particularly due to the new approaches to credit risk. Institutions face the challenge of efficiently managing their capital requirements in order to meet regulatory requirements while achieving their economic goals. With our CRR III 360° approach, we help you navigate the complexity of the new regulations.

Latest posts on Banking.Vision

CRR 360°

The CRR III 360° approach combines regulatory compliance with economic efficiency by offering comprehensive solutions for optimizing capital requirements and risk management. With our expertise, we support banks in meeting the complex requirements of CRR III – sustainably and strategically.

Your contact person

heads the Finance & Capital Markets division and advises on topics such as overall bank management, LCR management, reporting and liquidity risk management.